Y H & C Investments April 2025 Update

Sturgeon's Law Has Merit

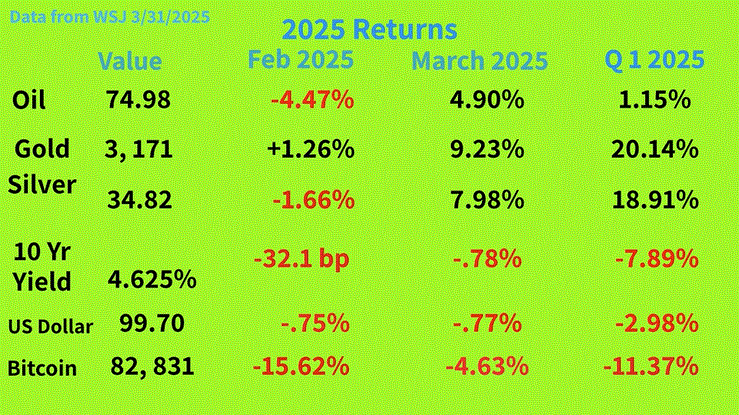

Y H & C Investments- Sturgeon’s Law Applied to Markets

(Return figures come from the March 31, 2025, edition of the Wall St. Journal. Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives)

Making good decisions is important, not just in markets, but life. A big part of making intelligent, thoughtful, and well considered decisions is evaluating all of your choices relative to others. On this note, let us turn to Sturgeon’s Law. It comes from Theodore Sturgeon, a noted science fiction author. In 1951, at a talk at New York University, he stated, “It came to him that [science fiction] is indeed ninety-percent crud, but that also – Eureka! – ninety percent of everything is crud. All things – cars, books, cheeses, hairstyles, people, and pins are, to the expert and discerning eye, crud, except for the acceptable tithe which we each happen to like.[4]”

Well, doesn’t that encapsulate decision making in a different light? Applied to financial markets and life, when nine out of ten choices are shall we say, sludge worthy at best, finding those that have legitimate merit requires quite a bit more effort. When the ratio of good to bad is one to nine, the total number you look at it needs to be large. For investors, the task is more daunting as we want to own things which yield a return on our capital which is better than not just a bank account, but also what one could earn by owning a market index. As part of this, we must consider other asset classes like cash, bonds, commodities, real estate, or if we are so fortunate to have access, venture capital and private equity. Throw in private credit, pre-public equity (privates), options and cryptocurrencies, maybe even stablecoins, and ooh boy, the challenge gets more interesting. Should we include online sports betting or event outcomes like Polymarket? Let’s leave that for another time.

Sturgeon’s law is an excellent and realistic observation which has to be considered with capital allocation. We want to own the best assets, and we want to buy them based on reasoning, analysis, and prices which we consider logical, factual, and attractive. In time, the worthiness of owning these will earn returns which will grow and yield acceptable results. The challenge for anyone is to keep expectations realistic and grounded in terms of results and time horizons. Everyone wants to earn excellent returns. However, the more one is concerned with results relative to the market, or even worse, other investor performance, the less attention is paid to what matters, which is making good decisions about what one owns.

Turning to the current financial environment, the unpredictable nature of markets was on display in March. With increased concern over a slowing economy and strained consumer purchasing power, global tariff considerations heightened volatility in equities and currencies. The lingering threat of inflation also contributed to negative investor sentiment. Many investors and corporations are also concerned about the lack of predictability with the new administration, which makes any kind of long-term planning quite challenging. I suspect the tariff unpredictability will resolve itself over the next six months or so. All are part of the ongoing challenges investors always face. Theodore Sturgeon’s analysis is as pertinent today as it ever was, and it is a principle to use in evaluating investment choices both today, and in the future.

Spanning the Globe: A Changing Globe as the Rest of the World Ponders a Trump Led US While Europe Opens the Purse

The nature of markets is ongoing change and the environment across the globe is illustrative of this. The two global powers which dominate the landscape, the United States and China, are at different points as they evaluate their national interests. President Trump is leading an approach which centers on restoring the manufacturing base and establishing an economy more concentrated on and amenable to the private sector. It includes less government spending and regulation, and more accommodative tax policy. As part of this effort, more aggressive tariff approaches relative to the international community have disturbed trading partners. Europe, Canada, Mexico, Brazil, and other South American countries face a trade picture which is reliant on exports into the United States. Increased scrutiny on international spending and foreign assistance calls into question how China views these actions. China suffers from a lingering recession, overcapacity in real estate, and slow domestic growth rates. It has extended credit across the globe as a way to help gain access to commodities which it depends on, especially energy. It’s neighbors in Asia like India, Japan, South Korea, the Philippines, and Australia, see an increasingly expansionist regime which has ties to countries which are often antagonistic at best, like Russia, North Korea, and Iran.

Across the pond in Europe, long time US allies and trading partners see a less dependable partner in terms of funding European defense from aggressive countries, specifically Russia. Germany recently elected a new Chancellor and enacted changes to its debt policies allowing for defense and security spending to be exempt from debt restrictions. It also creates a $545 billion dollar infrastructure fund. For the EU, Goldman Sachs estimates show defense spending to rise from 1.8% of GDP in 2024 to 2.4% by 2027. It amounts to a little under $100 billion per year increase. Clearly, this is a dramatic change from what has taken place over the last thirty years. As one ponders the future, does the increase in defense spending across Europe mean the region has more of a case for investors than previously thought? If one wants exposure to the defense and security industries, obviously more spending is always better than less. Really going out on a limb there, aren’t I?

Looking ahead, the globe never seems more interesting than it does today. With an AI world in swing, private credit popularity is on the rise, and demand for raw materials to support utilities, data centers, and the move towards everything connected and electric are popular themes. With all the possibilities across the world, don’t forget our friend Theodore Sturgeon.

Y H & C Investments in April- A Very Busy Month

March was a productive month in the Y H & C Investments world. As mentioned in the last update, a few of our holdings benefited from activist investor stakes, and the theme continued with a buyout of an insurance company holding. It is the third largest medical malpractice insurer in the country, and it also has a regional workers compensation insurance segment. It was bought out by the second largest medical insurer, a private company. The deal is scheduled to close next year. We have owned this for about five years or so. There is still a small arbitrage opportunity left in it so we will see how it plays out.

Markets have become difficult over the last six weeks, and challenging periods are excellent for finding out how investors feel about your holdings. It really shines a light on the shareholder bases of what you own, especially in the small and mid-sized areas. With larger holdings, they usually have very liquid instruments so institutions can easily enter and exit as needed. Much depends on the capital structure and how much is owned by management and insiders versus the rest of the investment community. It is why analyzing capital structures and shareholder ownership is an important part of investment analysis. Elsewhere, quite a few of our smaller companies reported results. Each has a unique situation and expect a solid 2025 with everything the same as far as business model and approach. Increasing revenues, improving margins, reinvesting into growth areas, and being smart and opportunistic about capital allocation are all consistent themes across the holdings. The key point is to monitor results versus the plans to compare what is accomplished and what is projected. April is a very busy period as I will be in New York for the LD Micro Conference and then attend the Planet Microcap Conference here in Las Vegas later in the month. Thank you for reading the April update, I really appreciate it. If you have any investment questions, please reach out to me at information@y-hc.com. I hope you have a great month.

Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives)