Y H & C Investments March 2024 Update

Dealing With the Cray Cray-

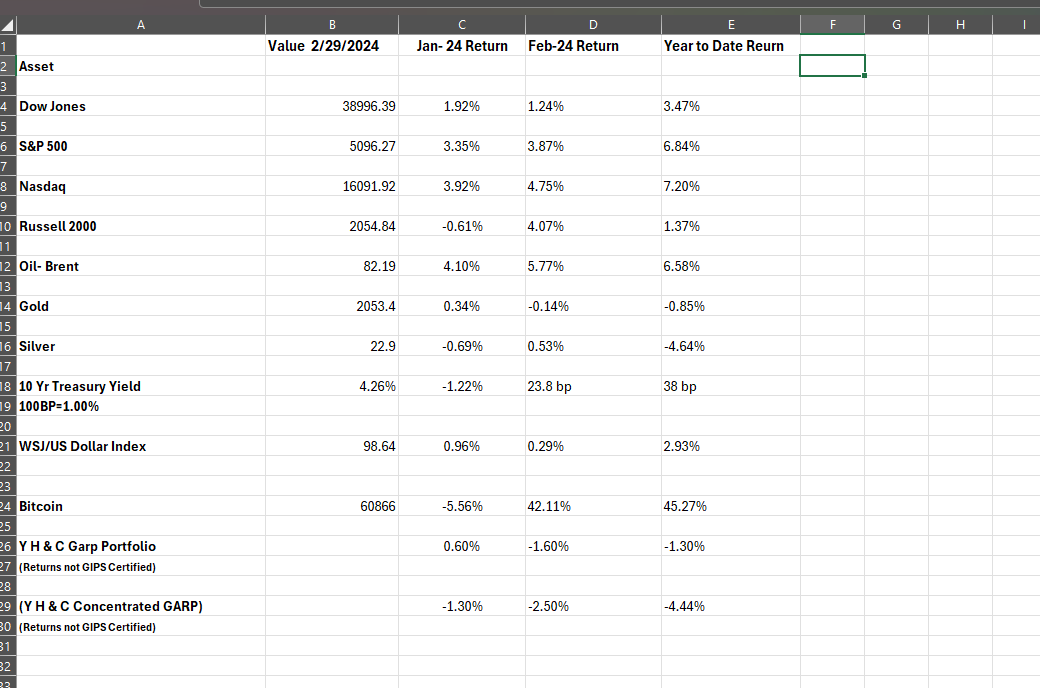

February 29, 2024

Ignoring the Cray Cray, and What to Choose in the Magnificent 7 Era!

Return figures in this section come from the January 30, 2024, edition of the Wall St. Journal. Y H & C Investments may have positions in companies mentioned in this newsletter. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives)

The Super Bowl game between the Kansas City Chiefs and San Francisco 49rs was the highest watched game ever. During the game, held here in Las Vegas, a person decided to run onto the field naked and draw attention to their, well, freedom of expression. A similar thing happened in the prior year’s Super Bowl, too. The modern term for these individuals would be Cray Cray, meaning crazy. Loons. Nuts. Disturbed individuals. We don’t know how they got this way, or what made them feel so inclined to share their feelings in such an obviously misguided manner. I mention this because of the similarity to what takes place in capital markets.

Every day, people make decisions about how they allocate capital. We have no idea what factors into their actions. Each entity has their own situation of which they are aware. With diverse kinds of investors, there are different goals and constraints which affect how they approach investing. On the institutional level, matching assets to liabilities is usually a priority, but not always. Historically, when failing to do so, it has been the source of major problems. Leverage is also usually involved with financial trouble. In today’s market, algorithms are much of the trading volume. The current approach is based on momentum, or whatever works will continue to work. Consequently, what continues to get bought is what has been working. It is the financial markets version of the Cray Cray. I have no idea how long it will continue but it is not my approach. My friends and clients, one and the same, are familiar with the way I go about investing. Still, we must recognize the challenge of only ten stocks outperforming as clients want their money to grow. So how do we deal with an outrageously top heavy market environment?

The answer is to create portfolios with assets which are not dependent on the financial markets. It means they don’t have to go to the capital markets to raise money. They use their profits to reinvest in the business, buy back stock, make acquisitions, or retire debt. The decision is based on what is the best alternative. It means you need very intelligent people who run these companies who have a large financial incentive to make smart decisions about how money is spent. In some cases, the business may be working towards this optimal situation. Over time, repeatedly making thoughtful decisions about how shareholder money gets allocated eventually gets rewarded. Note the term, eventually. As an example, if a company uses its cash generation capability to retire 5-7 percent of the outstanding stock every year, in 3-5 years from 15-35% of the available stock is reduced. Existing shareholders own much more of the same entity. If the company also grows its revenues, you own a greater piece of a bigger, more profitable business. If it does so while not incurring more debt, or potentially retiring debt, or refinancing debt at lower rates, value accrues to shareholders. None of this relies on what the algorithms are trading. If we add to this equation situations where there are a limited number of shares to begin with, it explains my approach to the Cray Cray environment.

One final note to keep your eye on. As an investor, it is important to be aware of systematic risks, meaning things which could dramatically impact the market. The biggest challenge to global markets is the weak financial position of the United States Government. It is reflected in the thirty-four trillion dollars of on balance sheet debt, probably 100 trillion total if off balance sheet is included. As part of this is nearly 2 trillion-dollar annual deficits. The counter argument is our higher GDP growth rate versus the rest of the world. I don’t think US GDP growth at above trend rate is sustainable in any way. The important question is how to invest to take advantage of massive US government profligacy? One answer is to go short dollar assets or buy cheap non-US assets. Make no mistake, the dollar issue is not going away any time soon.

Y H & C In February: Back to Basics

One of the difficult things about investing is there are so many kinds of instruments in which you can place your capital. In combination with the limit on available funds, client specific needs, and competition by firms with far more resources, the ability to create excellent returns is fierce. In thinking about this dynamic, I came back to the premise of building on the history of successful investments. Over the course of 30 years of investing, there have been plenty of wonderful results. However, the best returns have been found in areas where I have long been familiar with an industry. These areas include payment processing, consumer discretionary, financial services, health care, energy, merger arbitrage, and various segments of real estate.

As part of this focus, it is more important to be extremely specific on establishing the investment thesis for any investment. For me to have repeated success, a specific process is needed for every capital allocation decision. There is a difference between being correct on an investment decision because you went through a well-defined process, versus having a good result (maybe even great) based on a hunch or one or two reasons which just occurred to you. One of the realities about today’s market is that the largest companies like Microsoft, Amazon, Facebook, and Apple have created massive amounts of wealth for their shareholders. If you invested in these companies many years ago, your thesis may have been based on one specific premise. As examples, for Microsoft it may have been the operating system dominance or with Amazon their retail strength. Over the last decade, areas which had nothing to do with that, like Microsoft’s building of the cloud and consumer areas with acquisitions of LinkedIn and Activision, or Amazon’s web services and advertising, have surpassed the size and profitability of the original core business. Did investors have an open-ended thesis when they originally placed capital in those companies? If so, well done, and congrats.

As someone trusted with growing my client’s capital, being precise about why I am investing establishes the specific reason for putting capital in a company. It is extremely helpful when the stock inevitably declines because you go back to your thesis to see if anything has changed. Most of the time it has not. Focusing my attention on investment fundamentals and industries where I have a well-defined knowledge base are another way of dealing with the current market environment, one which is driven by capital flows and momentum. As a current example, our real estate holdings are diversified into a variety of segments. They include companies which are broadly diversified or specialized. Up until the last few weeks, with the market consensus of upcoming interest rate reductions, all areas of real estate benefited. Recently, as the cuts are now thought to have been pushed back, the real estate complex is now back in the doghouse. Has anything changed with the companies we own? No. It highlights the need for a comprehensive understanding of why we own what we do and why we should stick with it. The investment thesis and process anchor this knowledge.

Y H & C Industry & Holdings Update- Focus on Capital Allocation! (YH & C Investments may have positions in companies mentioned in this newsletter. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives)

In February, my time was spent reading transcripts of earnings reports and the subsequent conference calls. We have companies in a wide variety of industries which are generating cash and reinvesting most of it to grow the business. The amount of cash each company produces is obviously different. In some cases, especially for smaller companies, all the profits are reinvested. Larger companies may be buying back stock, retiring debt, and paying dividends. Depending on the classification, there can be restrictions on what a company must do with its profits. As an example, real estate investment trusts must distribute 90% of their annual taxable income to investors for dividends. Nearly all our smaller companies have yet to report earnings as they are due in the next few weeks.

Many famous investors in the investment management business believe the mark of a true professional is evaluating the risk of an investment relative to the reward. The focus is on measuring what could go wrong versus the gain if you are correct. This approach is well advised. My own opinion is a little different. The biggest mistakes I have made involve selling stock too soon. Failing to anticipate what can go right and how much enthusiasm markets may have for a wonderfully performing company is incredibly costly in terms of the lost value created by not owning well-performing entities.

Finally, over the last few months, I spent time rethinking how I go about marketing my company. I have a new web site which emphasizes the fact that Y H & C was built with an investment focus. I invest in individual companies. For my friends and clients, our success is something I am immensely proud of, and the web site reflects those stories (in a non-revealing way, of course). It also highlights areas of professional expertise, tax planning and retirement accounts, clients benefit from. I worked with Treyton Devore, who is an incredibly talented guy who I highly recommend. You can reach him at treyton@piertree.com. He specializes in financial sites but is honorable and will make your vision come to life. If you are interested in what mine is or how I can potentially help you, please visit www.y-hc.com. Any feedback is always appreciated. Thanks for reading the monthly update, and if you have questions or situations I need to know about, please email me at information@y-hc.com

If you think it is worthy, recommending this edition to a friend or family member would be appreciated.

(Y H & C Investments may have positions in companies mentioned in this newsletter. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives. Past performance is not an indication of future results, and you may lose your principal by investing in stocks.